Numbers Report – July 03, 2026

In the latest edition of the Numbers Report, we will take a look at some of the most interesting figures put out this week in the energy and metals sectors. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers.

Let’s take a look.

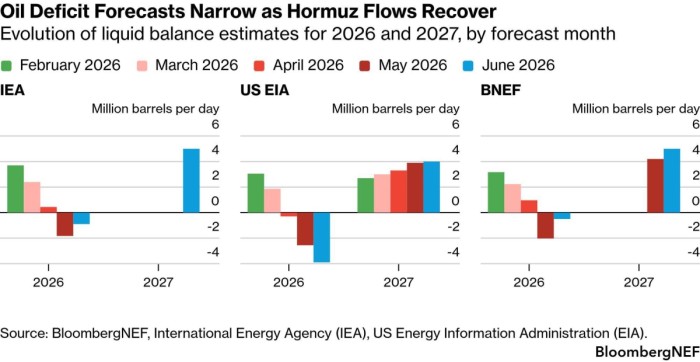

1. Hormuz Turns Oil Outlooks Into a Guessing Game

– Energy market research organizations have started to recalibrate their global supply outlooks for 2026 and 2027, with the US Energy Information Administration seeing a much slower return of production than the IEA or Bloomberg’s NEF.

– In their June monthly updates, the IEA and BNEF narrowed their 2026 deficits to 900,000 b/d and 500,000 b/d, respectively – both predicted a 2 million b/d supply shortfall a month earlier.

– The EIA, on the other hand, stated that it doesn’t expect a Hormuz recovery to pre-war levels before early 2027, expecting global oil inventories to fall by an average of 7.6 million b/d in Q3 2026.

– Whilst all market forecasters expect 2027 balances to be wildly skewed towards a supply glut, the discrepancies between short-term outlooks are staggering.

– The monthly Reuters poll on oil price projections saw the 2026 Brent average fall back to $84.5 per barrel this month, down $6 per barrel compared to May, suggesting the analytical community is reactive and has no real read on what the US or Iran will do next.

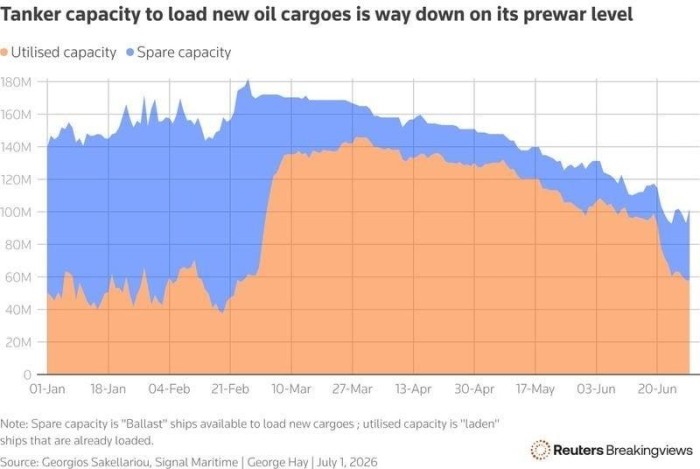

2. Hormuz Traffic Rises, But the Shipping…

Numbers Report – July 03, 2026

In the latest edition of the Numbers Report, we will take a look at some of the most interesting figures put out this week in the energy and metals sectors. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers.

Let’s take a look.

1. Hormuz Turns Oil Outlooks Into a Guessing Game

– Energy market research organizations have started to recalibrate their global supply outlooks for 2026 and 2027, with the US Energy Information Administration seeing a much slower return of production than the IEA or Bloomberg’s NEF.

– In their June monthly updates, the IEA and BNEF narrowed their 2026 deficits to 900,000 b/d and 500,000 b/d, respectively – both predicted a 2 million b/d supply shortfall a month earlier.

– The EIA, on the other hand, stated that it doesn’t expect a Hormuz recovery to pre-war levels before early 2027, expecting global oil inventories to fall by an average of 7.6 million b/d in Q3 2026.

– Whilst all market forecasters expect 2027 balances to be wildly skewed towards a supply glut, the discrepancies between short-term outlooks are staggering.

– The monthly Reuters poll on oil price projections saw the 2026 Brent average fall back to $84.5 per barrel this month, down $6 per barrel compared to May, suggesting the analytical community is reactive and has no real read on what the US or Iran will do next.

2. Hormuz Traffic Rises, But the Shipping Bottleneck Remains

– Tanker transit data have become the most immediate gauge of US-Iran diplomacy, with shipping activity through the Strait of Hormuz recovering compared to March-May levels, however still far below pre-war readings.

– In the week to June 28, transits through the Hormuz reached 242 vessels across all tanker types, well below the 700-plus average of 2025.

– The release of nearly 100 million barrels of previously stranded crude has temporarily eased prices in the physical market, with ICE Brent, Dubai, Murban and INE Shanghai all flipping to a contango in recent weeks.

– That said, up to 9 million b/d of Gulf production may still be shut in because exporters cannot secure enough tankers, suggesting recovery would take longer than previously expected.

– Chartering ships out of the Gulf remains an expensive endeavour – even though Middle East-to-China freight rates have fallen in recent weeks, at $315,000 per day they are more than triple the normal market level.

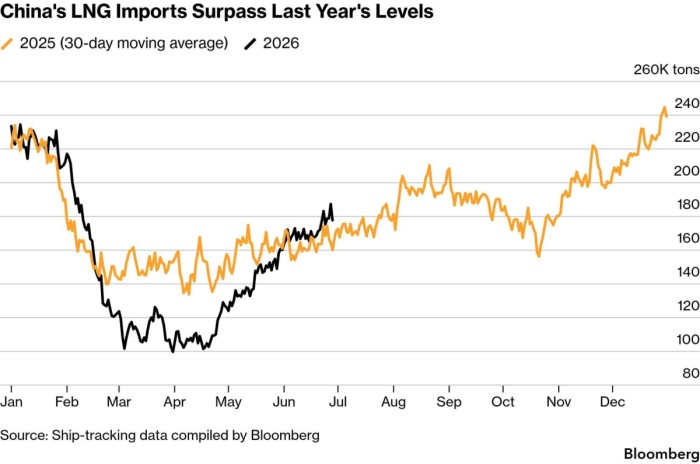

3. China’s LNG Recovery Runs Into a Hot, Expensive Summer

– China’s LNG imports have been gradually recovering since the US-Iran conflict disrupted global energy flows, with June inflows coming at 4.9 million tonnes, only slightly lower than year-ago levels.

– Beijing’s rising appetite for LNG is stemming from lower domestic production (due to offshore disruptions and field maintenance) and depleting inventories amidst re-emerging heatwaves.

– Chinese gas inventories are currently around 45% full, with a full-fledged replenishment hampered by high LNG prices and blistering temperatures, particularly in the south.

– Australia’s share in China’s LNG imports has jumped to 36% on the back of stranded Qatari supply, the highest reading on record.

– Russia, currently the third-largest LNG supplier to China, could further boost imports in July-September as the Northern Sea Route navigation season has opened with 3 LNG carriers already underway, en route to Chinese buyers.

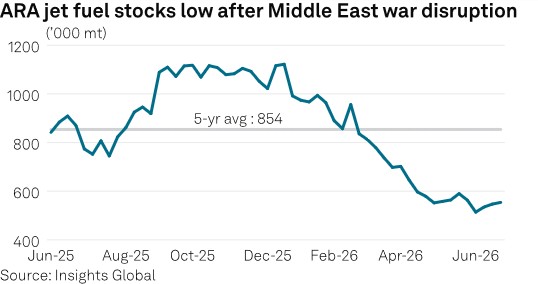

4. Europe’s Jet Fuel Panic Cools, But the Tanks Stay Thin

– European jet fuel prices have now almost halved compared to their April 2026 runaway levels, the Old Continent is still weighing the possibility of supply shortages ahead.

– The price of jet fuel in Northwest Europe has dipped to $970/mt this week, whilst current pricing levels in the Mediterranean trend around $940/mt, a fraction of the $1,842/mt peak posted on April 2.

– Europe has so far managed to avoid supply shortages, even though regional inventories remain wafer-thin, with ARA stocks plunging to just 554,000 tonnes in the week ended June 25, 50% below pre-war levels.

– The backwardation of the jet fuel forward curve seems to suggest that, for the time being, Europe’s refiners are confident peak summer demand will be met, with August forwards trading some $20/mt below July.

– That said, if all the vessels currently stuck in the Gulf cannot make it through the Hormuz over the upcoming days, sentiment could sour again as Europe’s September needs remain largely unmet.

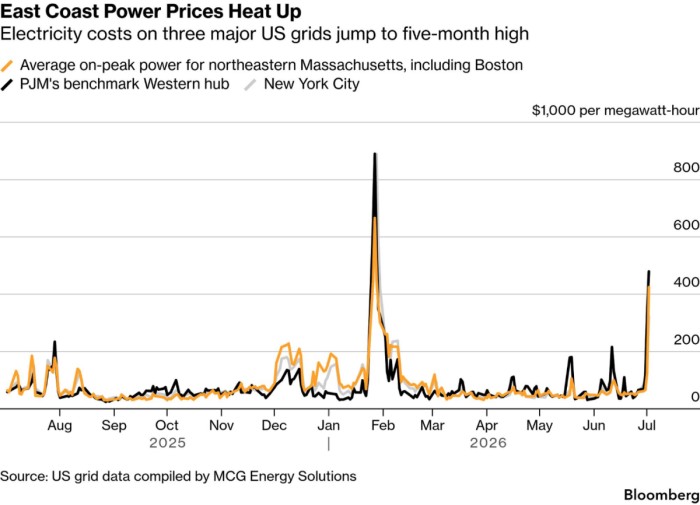

5. East Coast Heatwave Puts America’s Power Grid on the Grill

– Sweltering heat across the US East Coast could sour the mood for the upcoming Independence Day holiday as electricity prices from New York to Virginia are soaring.

– Day-ahead power prices in New York jumped above $1,100 per MWh on Wednesday as temperatures started to climb towards 100 F (38 C), marking the worst strain on grids since Winter Storm Fern.

– Exacerbating the power squeeze, a recently completed power line designed to bring hydropower from Quebec to New York shut down for a day due to a ‘technical issue’.

– According to preliminary data, the country’s largest grid – PJM Interconnection – surpassed its previous all-time peak load record of 165.5 GW on Thursday, a record that has been in place since 2006.

– With data centres boosting the needs of East Coast grids, operators were told to maintain reliable operations as a priority as the Department of Energy allowed them to sidestep some environmental mandates to keep power coming.

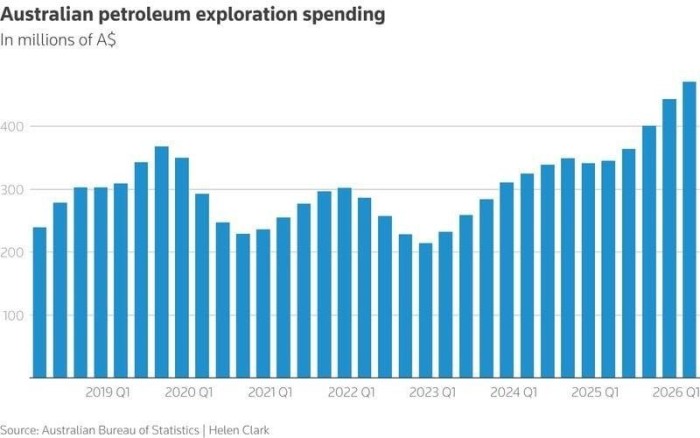

6. Australia’s Gas Drilling Boom Meets Canberra’s Gas Grab

– Australian oil and gas exploration spending reached a 10-year high of A$471 million in Q1 2026, just as Canberra frightened regional energy companies with its 20% domestic gas reservation rules.

– Ahead of its re-election in 2025, the Albanese government promised to facilitate new gas supply, admitting that by the end of the 2020s Australia would face regional shortages.

– Following years of drilling that mostly focused on onshore plays, activity is now increasingly shifting towards the offshore, such as the Otway Basin, however the largest untapped resources are still onshore.

– Australia’s 2nd largest producer Santos is drilling three appraisal wells in the Beetaloo Basin, in the central-northern part of the country, seeking to tap into shale deposits, utilizing multi-stage fracking technologies.

– The pace of exploration could decline notably should Canberra’s gas mandate frighten investor capital, with smaller companies particularly wary of gas reservation requirements.

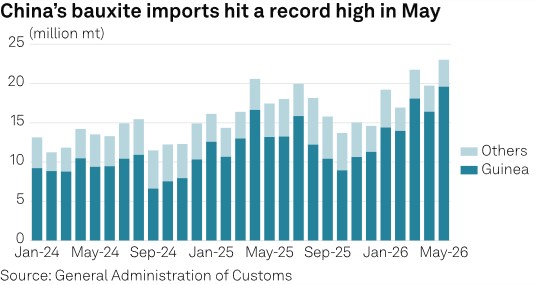

7. China’s Guinea-Fuelled Bauxite Boom Starts to Fade

– Chinese interest in bauxite imports has started to falter after an exceptionally strong start to 2026 purchases, mostly driven by an export boom from Africa’s leading producer, Guinea.

– Guinea supplied 19.61 million metric tons of bauxite to China in May, accounting for 85% of the country’s total inflows, as Chinese alumina producers accelerated purchases ahead of possible Guinean export restrictions.

– Market speculation has indicated Guinea could cap its bauxite exports at 150-170 million metric tonnes per year; however, up until now, the African country has yet to publicly release a final framework.

– Meanwhile, aluminium prices continued to decline to their lowest in five months, with the LME three-month benchmark touching $3,040 per tonne this week on expectations of improving supply once the Strait of Hormuz reopens.

– Adding downside pressure to prices, the UAE’s Emirates Global Aluminium announced that it would restart production at its drone-damaged Al Taweelah complex earlier than previously assumed.

That’s it for this week’s Numbers Report. Thanks for reading, and we’ll see you next week.